Published February 16, 2024Edited May 12

The sustainability of the streaming sector has been called into question repeatedly over the last few years. However, beneath the headline-grabbing gloom lies the launchpad that could catapult major studio streamers to profitability in likely a relatively short space of time. Indeed, over the course of the next two years, a combination of cost rationalization, revenue diversification and content monetization could make streaming not only viable but also a major profit driver for the U.S. studios.

The well-publicized cutbacks in staffing and in wider global operations, though disheartening at a personnel level, represent a clear move toward reducing overhead costs. They also better reflect more streamlined working practices within businesses that had arguably become bloated in the hunt for subscriber growth.

With many mature markets reaching the point of subscriber saturation, the streamers’ focus has changed from new subscriber acquisition to subscriber retention. Managing churn is a major challenge for streaming services; consumers are presented with a greater volume of services than ever before. The structure of monthly subscriptions, rather than longer-term contacts, enables users to switch between services far more readily and arguably encourages them to chase the new original content zeitgeist. Ampere Analysis’ own research shows that churn rates for streaming services are 14% per year at best, with most services enduring much higher rates.

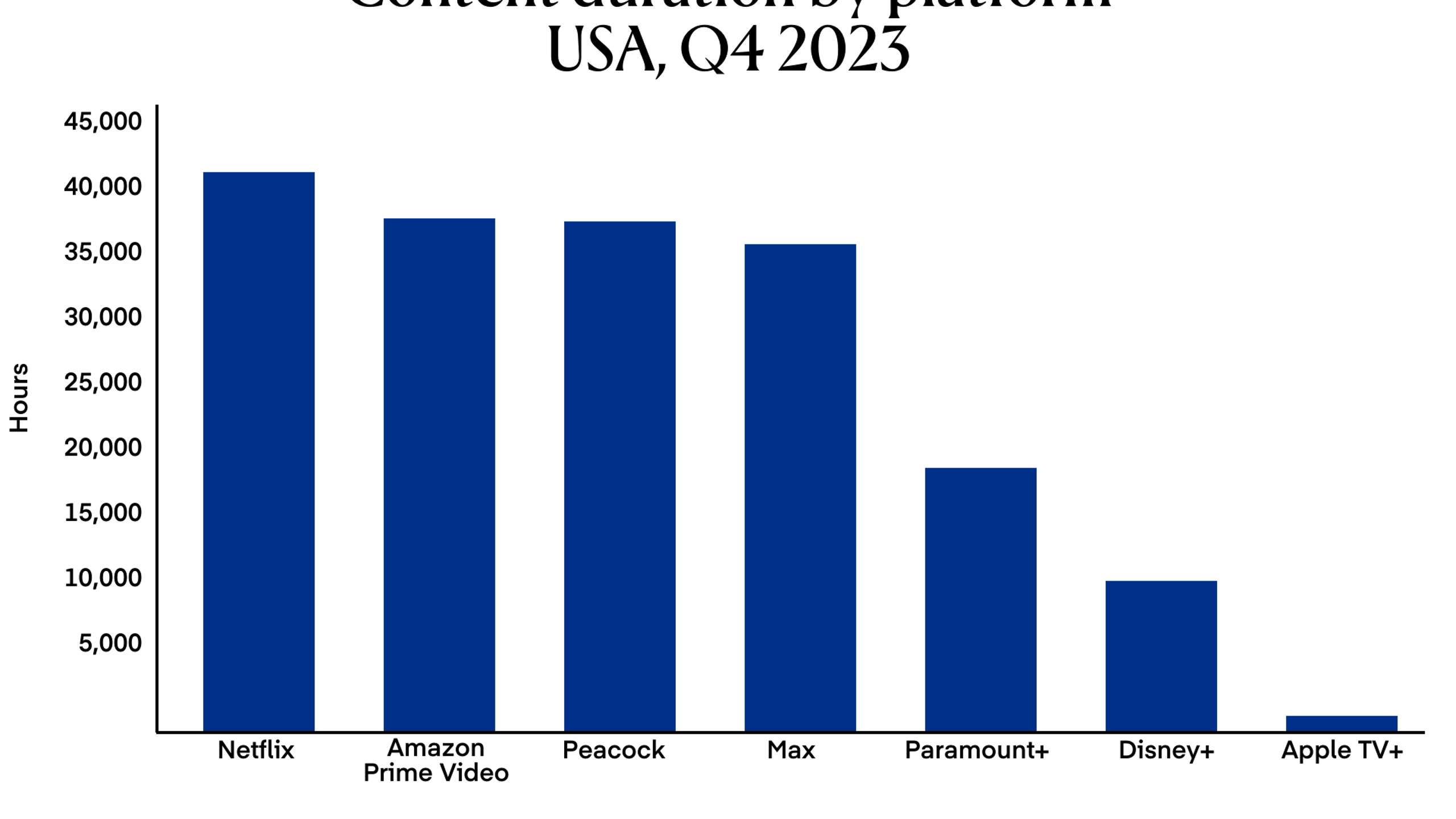

Ampere’s analysis has shown that larger catalog sizes can have a positive effect on reducing churn. However, a careful balance needs to be struck between offering sufficient content, whereby subscribers’ more passive viewing needs can be met, and overwhelming those same subscribers with a surfeit of choice. Filling streaming catalogs with older and lower-quality content (while perhaps a solution for some free, ad-funded video on demand providers) is not a viable solution for paid streaming services. Indeed, despite the vast content catalogs at their disposal, the volume of available titles on services such as Disney+ remains tightly curated, reflecting a more nuanced content mix. The studios have to strike a careful balance between lowering content investment so they don’t overspend and erode their emerging profit margins, and funding enough new content to enable subscriber retention.

A primary focus on high-quality scripted content, once the mainstay of streamers’ commissioning, has given ground somewhat to a more equitable split of less expensive unscripted content, including reality and entertainment shows. These represent a high volume of low-cost viewing hours which, while not necessarily destination viewing, helps retain subscribers by providing greater content-viewing hours.

The same is true on the scripted side, with an increased focus on crime procedurals, which both extend viewing time and typically attract older subscribers. In addition to these and other changes in catalog mix, streamers have adopted the episodic release schedules of their linear TV predecessors in order to extend the time that consumers are engaged in and subscribed to their platform.

It is not only in their streaming services where the U.S. studios have reassessed their approach to content. In more recent months, there has been a clear recognition that streaming is not the only way to monetize their content, with the revival of content windowing and licensing. Studios have brought back their theatrical and pay-TV windows, as well as the practice of licensing their catalogs to other platforms and territories, to maximize the value of their content across the whole distribution chain.

Outside of the content offering itself, the drive to profitability has prompted increases in subscription pricing, which can increase churn. However, the introduction of advertising tiers across almost all the major studio streaming services in the past year provides a means by which existing subscribers can continue to use services at the same or even lower monthly cost.

Ampere’s own analysis of these developments indicates that price increases still lead to customers churning, but the impact is short lived and less marked in services where there is an option for same or lower-priced ad-supported viewing. The presence of a same-cost ad-supported tier not only reduces churn, but also encourages more ad-averse consumers to upgrade to higher-priced ad-free subscriptions. Further to this, the presence of a lower-cost ad tier not only lowers the entry barrier for consumers who are reluctant to pay for multiple services, but also adds significant growth potential to the streaming market. Our current forecasts suggest that streaming advertising could grow revenue by 68% between 2023 and 2028, compared to 28% growth for subscription revenue alone.

With these adjustments, the studios have likely set themselves on a path to profitability that is both consistent across the studio players and also quite imminent. Ampere’s models project that all the major studio streamers will reach quarter-on-quarter profitability by the first quarter of 2025. This breakthrough moment could come faster to the large and more mature services, with Disney and Warner Bros. Discovery likely to be reporting profits as soon as the end of 2024. By year end 2028, we expect the studio streaming businesses will generate a combined profit of more than $6 billion.

However, imminent profitability does not mean that streaming will be easy or risk-free. With incumbent steaming-only players and tech-supported services offering fierce competition, the studios will need to remain steadfast in their innovation.

This op-ed represents the views and opinions of the author and not of The Current, a division of The Trade Desk, or The Trade Desk. The appearance of the op-ed on The Current does not constitute an endorsement by The Current or The Trade Desk.